There have been several developments in recent days concerning the US and European economies. In the light of my past articles about our economic crisis, I'll note the most important ones here. Yes, the light at the end of the tunnel IS an oncoming train, economically speaking.

1. Half of US mortgages are effectively underwater.

According to CNBC:

On US totals, if you figure average house prices use conforming loan balances, then a repeat buyer has to have roughly 10 percent down to buy in addition to the 6 percent Realtor fee to sell. Thus, the effective negative equity target would be 85%. You also have to factor in secondary financing, which most measures leave out.

Based on that, over 50 percent of all mortgaged households in the US are effectively underwater — unable to sell for enough to pay a Realtor and put a down payment on a new purchase without coming out of pocket. Because repeat buyers have always carried the market as the foundation, this is why demand has not come back. It's as if half the potential buyers in America died over a two-year period of time.

More at the link. Bold print is my emphasis.

2. The US government is planning to cheat us all by tinkering with inflation statistics - again.

The Tennessean reports:

Just as 55 million Social Security recipients are about to get their first benefit increase in three years, Congress is looking at reducing future raises by adopting a new measure of inflation that also would increase taxes for most families — the biggest impact falling on those with low incomes.

If adopted across the government, the inflation measure would have widespread ramifications. Future increases in veterans’ benefits and pensions for federal workers and military personnel would be smaller. Over time, fewer people would qualify for Medicaid, Head Start, food stamps, school lunch programs and home heating assistance.

Taxes would go up by $60 billion over the next decade because annual adjustments to the tax brackets would be smaller, resulting in more people jumping into higher tax brackets. Annual increases in the standard deduction and personal exemptions would become smaller.

Despite fierce opposition from seniors groups, the proposal is gaining momentum in part because it would let policymakers gradually cut benefits and increase taxes in a way that might not be readily apparent to most Americans.

Again, more at the link.

This is merely the latest government 'fiddle' in a long, long line of them, where they've adjusted the measurement of inflation to their advantage, and our cost. As John Williams of Shadow Government Statistics points out:

The key is how you define consumer inflation. I operate on the premise that the post-World War II CPI concept of inflation measured based on a fixed-basket of goods -- a measure of the changes in prices related to maintaining a constant standard of living -- was a reasonable, meaningful and useful approach for most consumers.

Some years back, then Fed Chairman Alan Greenspan began making public noises about how the CPI overstated inflation. Where the fixed-basket of goods approach would measure the cost of steak, year after year, Mr. Greenspan argued that if steak went up in price, people would buy more hamburger meat, mitigating the increase in their cost of living. The fact that switching the CPI concept to a substitution-based basket of market goods from a fixed-basket violated the original intent, purpose and concept of the CPI, never seemed to be a concern to those in Washington. Artificially reducing reported CPI inflation would have a variety of benefits, beginning with reduction of the budget deficit due to the cutting of cost-of-living adjustments for Social Security payments.

Accordingly, geometric weighting was introduced to the CPI reporting methodology, which had the effect of mimicking a substitution basis. Since the revised CPI still did not show as low an inflation rate as a fully substitution-based index would, Mr. Greenspan began focusing the Fed's inflation targeting and measurement on the inflation rate used to deflate personal consumption expenditure (PCE) in the GDP. Such was a substitution-based measure.

More recently, the BLS [Bureau of Labor Statistics] introduced the Chained CPI-U (C-CPI-U) as an experimental substitution-based inflation index, which closes follows PCE inflation.

Yet, as oil prices began their current uptrend, substitution-based inflation reporting still was not low enough for the former Fed Chairman, as he began embracing the concept of "core" inflation, inflation net of food and energy price changes. Eliminating bothersome price increases in energy and food products -- such as seen with oil at present -- would make the Fed's job of containing reported inflation all the easier.

In general, if a government economic measure does match common public experience, it has little use outside of academia or the spin-doctoring rooms of the Fed and Wall Street.

. . .

... the new SGS Alternate Consumer Inflation measure ... reverses the methodological gimmicks of the last 25 years or so, plus an adjustment for the geometric weighting that is not otherwise accounted for in BLS historic bookkeeping.

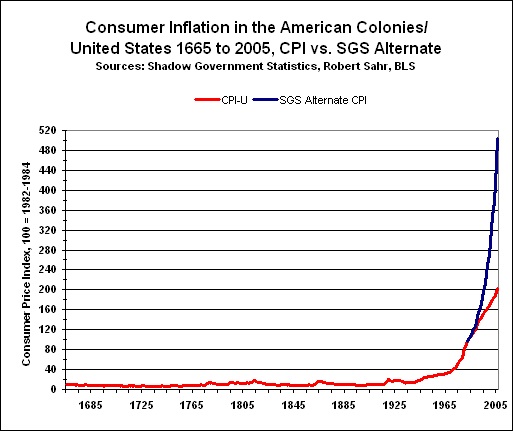

More at the link. According to Mr. Williams' SGS Alternate CPI, real inflation is running at over 11% on an annualized basis, compared to the 'official' figure of less than 4%, as illustrated in the chart below.

Needless to say, any increase granted by the US government in social security, pensions, etc. will be based on their much lower figure - not the figure calculated by Mr. Williams. Guess whose figures I believe? If you said 'the government's figures', I have this bridge in Brooklyn, NYC I'd like to sell you. Cash only, please, and in small bills. Just look at how government 'fiddling' with the numbers has altered the historical graph of inflation since the establishment of colonies in North America.

You'll notice how inflation generally picks up after the dollar becomes a fiat currency in the 1930's, and how it accelerates from the 1960's. Note the divergence between SGS's inflation figure and the government's after the latter began 'tinkering' with the formula used to calculate it. Needless to say, SGS's figure is much more accurate!

So now, the US government plans to give us a 3.6% increase in social security and other inflation-linked payments . . . while the real rate of inflation is more than three times higher. Furthermore, they want to tinker with the calculation of inflation even more, to reduce future increases. That's great for the Fed and the bureaucrats and the politicians, but it sucks to be us, I guess.

3. The US government's new measurement of poverty doesn't actually measure poverty as such.

Instead, it measures disparity of income - and it'll be used as a political tool, to justify the redistribution of wealth from the richer to the poorer. Hot Air reports:

Economists on both the left and the right have long had concerns and criticisms about the accuracy of the poverty rate — so, at the instruction of the federal government, the Census Bureau developed a new measure to determine the number of poor in America. The Bureau today released the nation’s poverty numbers under the new gauge.

Called “The Supplemental Poverty Measure,” the new indicator suggests 49.1 million Americans face poor economic conditions, compared with just 46.6 million under the standard measure. That sounds “grim,” as an MSNBC headline put it — but, just as the standard measure is misleading in many ways, so, too, is this new indicator.

“The new measure places income thresholds for poverty on a built-in escalator that rises automatically in direct proportion to any improvement in the living standards of the average American,” Heritage Foundation expert Robert Rector said in a statement. “So even if the real income of every single American were to double, the new measure would show no drop in poverty because the income thresholds would also double. The result is that, over the long term, poverty can be reduced only if the incomes of the ‘poor’ are rising faster than the incomes of everyone else.”

. . .

What is, perhaps, saddest about these figures is that it obscures the picture of true poverty — both in the U.S. and in the world. Like so much of this administration’s rhetoric, it encourages class envy and tends to inspire dissatisfaction with what actually amounts to a pretty decent standard of living among some who qualify as “poor” by the government’s measures.

More at the link. It's important reading if you want to understand what's behind government redistribution programs.

4. Europe's on the brink of economic disaster.

- Greece is witnessing a prolonged run on its banks, which has just seen the biggest monthly drop ever recorded in bank balances (during September). Why? Because Greeks are squirreling their money away outside the country or buying hard assets, in anticipation of the economic crash everyone knows is coming. Why would any sane person leave their money in banks that are almost certain to fail?

- Italy's economy is 'mathematically past the point of no return', according to Barclays.

- The same Barclays report says the European Central Bank will be forced to print money in order to buy bonds from European nations on the brink of economic collapse. However, the head of Germany's Bundesbank, Mr. Jens Weidmann, rejects this option: "creating new money to prop up government finances 'undermines the incentives for sound public finances.' He said Tuesday that governments would then rely on the “sweet poison” of central bank financing rather than risk offending voters by cutting spending or raising taxes to reduce their deficits. ... Weidmann also rejected any use of gold or currency reserves held by the Bundesbank to help fund the eurozone bailout fund in its efforts to backstop troubled governments. He said that would be a 'clear violation' of the prohibition on central banks financing government spending." That sets the Bundesbank, the Eurozone's most powerful and influential national financial institution, on a collision course with the national banks of the weaker Eurozone nations. Guess who's going to win? Remember the Golden Rule . . . "He who has the gold, makes the rules". In this case, the Bundesbank has the gold.

Putting all those elements together should make for an interesting few days ahead in the Eurozone . . .

5. The US deficit reduction negotiations are a farce, because neither side is serious about them.

As Mark Steyn points out:

In 2011, the United States government took in $2.17 trillion but blew through $3.82 trillion — and that’s before Entitlement Armageddon shows up down the road. If you’re spending $4 trillion but only raising $2 trillion, you need to be cutting government in half or you’re not serious. Washington is not serious. Indeed, it’s far more frivolous than Athens.

The world has begun to figure out that the US political class is institutionally incapable of changing its ways, and cannot be diverted from the most expensive suicide in global history. Regardless of whether or not the downgrade wallahs are a bunch of shysters, nobody could seriously argue that the present finances of the United States merit triple-A status. Once that’s gone, the dollar’s status as global reserve currency is on the block. And after that what’s holding the joint up?

More at the link. Bold print is my emphasis.

Robert J. Samuelson has an excellent prescription for success - but I doubt whether the politicians on either side, Democrat or Republican, are interested in reading what he has to say. They're too busy fiddling while Rome burns.

Peter

1 comment:

Wait, wait, wait. You mean to tell me that the government might be lying about inflation? UNPOSSIBLE!

I'm also very interested in this bridge you speak of...

Post a Comment